GAP Inc. A Time of Change and New Opportunities

Stability, Digital Growth, and Global Brands as the Key to Success in Retail

The Gap, Inc. (Ticker: GAP) is a well-established global retailer specializing in apparel, accessories, and personal care products. With iconic brands like Old Navy, Gap, Banana Republic, and Athleta, the company caters to men, women, and children. It operates through a mix of company-owned stores, franchises, and online channels. Founded in 1969 and headquartered in San Francisco, GAP has seen both highs and lows, with recent efforts focused on restructuring and regaining market share

Please read this first:

Financial reports GAP. inc

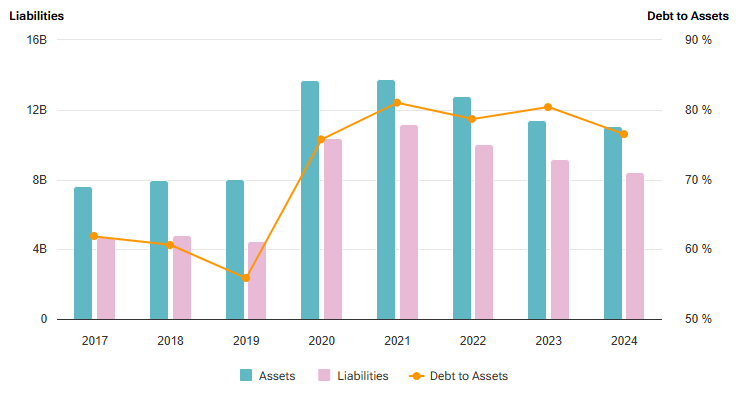

Balance Sheet:

Let’s start with cash. $2.2 billion. That’s no small amount, and a 64% increase compared to last year is impressive, wouldn’t you agree? But what really caught my attention is that inventory levels dropped by 2%. At first glance, that might seem insignificant, but think about it—fewer off-season products mean fewer markdowns and lower storage costs.

Debts? Exact figures aren’t specified, but with that kind of cash reserve, it’s hard to imagine they’re struggling with obligations. Plus, the company plans to spend $500 million next year on digital platforms, store upgrades, and supply chain optimization. The main risks are tied to potential increases in debt levels and dependence on efficient management in an unstable economy. However, current indicators reflect a balanced approach to financial management.

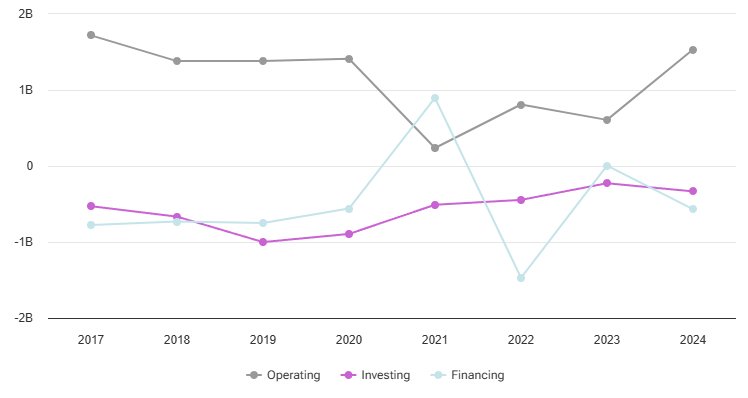

Cash Flow Analysis:

Here’s something worth noting: $870 million in operating cash flow is impressive. GAP isn’t just earning money; they know where to invest it. For example, they spent $330 million in the last quarter alone on improving digital infrastructure and logistics.

Free cash flow for the nine months totaled $540 million. That’s a reliable cushion that allows them to pay dividends and invest in growth. Speaking of dividends, $0.15 per share might not sound like much, but stability is key—and stability builds trust.

Capital:

Now, on to the capital structure: 373.5 million common shares outstanding, with a dividend yield of about 2.54%. It’s not groundbreaking, but for those seeking stable income, it looks reliable. EPS for the quarter stood at $0.72, proving the company’s profitability remains strong despite potential share dilution.

What’s interesting is the absence of significant insider trading or share buybacks. This could suggest that management is confident in its strategy, or perhaps they’re just waiting for the right moment.

Income Statement Analysis:

Revenue grew 2% year-over-year, reaching $3.8 billion for the quarter. But what’s truly impressive is that 40% of these sales now come from online channels. To me, that’s a clear signal that GAP understands where the future is headed.

Brand Breakdown:

Old Navy: Revenue reached $2.2 billion (+1% YoY). Comparable sales remained flat.

Gap: Revenue was $899 million (+1% YoY). Comparable sales increased by 3%, signaling steady brand momentum.

Banana Republic: Revenue stood at $469 million (+2% YoY). Comparable sales dropped by 1%.

Athleta: Revenue reached $290 million (+4% YoY). Comparable sales rose by 5%, driven by successful new products and marketing efforts.

Profitability is another highlight. Gross margin improved to 42.7%, and operating margin rose to 9.3%. These aren’t just good numbers—they’re proof that the company is running more efficiently. And $274 million in net profit confirms that they’re not just surviving—they’re thriving.

Management and Governance:

GAP appears to have a strong team in place. They’re betting big on e-commerce and brand refreshes.

For shareholders, this is good news too. Steady dividends, reinvestment into growth, and transparent communication all build trust. In a world where surprises happen at every turn, this kind of clarity is a real advantage. However, for many investors, an increase in the company’s stock value remains crucial.

Overall:

It seems that GAP Inc. is moving in the right direction. They have strong cash flow, improved margins, and are investing in the company’s future. But is that enough? The company is showing signs of operational recovery and margin growth. There’s significant growth potential if sales continue to rise and the economic situation stabilizes.

Short-Term Outlook: If they maintain their current pace, the stock could reach $30–$35, especially with sustained margin growth.

Long-Term Outlook: For dividend-focused investors, stability and e-commerce growth look attractive.

That said, retail is an industry where everything can change in an instant. Keep an eye on seasonal trends and key management decisions to stay ahead.

Strengths: Recognizable brands, solid cash reserves, and online sales growth.

Weaknesses: Dependence on seasonal sales and weaker performance in some segments (looking at you, Banana Republic).

Opportunities: Digital transformation and global expansion.

Risks: Economic instability and fierce competition.

Current Market Metrics

Current Price: $23.61

P/E Ratio: 10.93 (Attractive valuation compared to industry average of ~17.7)

52-Week High: $30.17

52-Week Low: $17.97

Dividend Yield: Not available (Dividend policy may not currently support income investors)

Short-Term Investment Strategy

Entry Point: Consider buying if the price drops to the $22.50-$23.00 range, close to its support level of $23.25.

Exit Point: Target a short-term exit around $25.45, the nearest resistance level, for a quick ~8% profit.

Risk: Short-term RSI (Relative Strength Index) at 33.4 suggests the stock is nearing oversold territory, but weak momentum could delay recovery.

Long-Term Investment Strategy

Entry Point: Accumulate shares under $24.00 to capitalize on long-term growth potential.

Valuation: With a forward EPS of $2.04, the stock trades at an attractive forward P/E of ~11.5, suggesting upside potential.

Exit Point: Hold for a 12-18 month target price of $30, assuming GAP executes its turnaround strategy effectively.

Risk: Sluggish recovery in retail demand or failure to differentiate its brands could cap gains.

Why Buy: GAP is undervalued relative to its peers, with a P/E ratio of 10.93 and a PEG ratio of -1.97, signaling that its current price does not fully reflect its earnings potential. Analysts have revised earnings estimates upward, and management changes, such as new leadership, could spark a turnaround.

Why Be Cautious: The retail sector is volatile, and GAP's historical struggles with inventory and brand positioning cannot be ignored. Macroeconomic factors like consumer spending trends will play a critical role in its recovery.