Grab: Secrets of Leadership in Southeast Asia

How a Local Startup Outpaced Uber and Became a Symbol of Innovation in the Region

When I look at Grab (Ticker: GRAB), I can't help but wonder: how does a company from Southeast Asia not only compete with global leaders like Uber but sometimes even surpass them? What kind of magic lies behind these results? Seriously, can their "secret recipe" be uncovered? Let’s figure it out.

The Beginning

Imagine two friends, Anthony Tan and Tan Hooi Ling, sitting in a Harvard lecture hall, deciding to change the world. They create a business plan, enter a competition, and only win second place. Doesn't sound very impressive, does it? But this was the starting point for Grab. The problem they wanted to solve was painfully familiar to every Malaysian: the poor quality of taxi services. Local taxi drivers violated rules so frequently that the country earned the dubious reputation of having the worst taxis in the world. Anthony and Tan decided: "Enough is enough; let’s change this!"

Grab was born out of the idea to improve the transportation system in Southeast Asia, making it accessible, safe, and convenient. It wasn’t just a startup; it was a challenge to the status quo. And this was just the beginning of their journey.

Please read this first:

Financial reports GRAB

Unique Approach

Let’s be honest: Uber, as a global giant, wasn’t the ideal solution for local Southeast Asian markets. Could anyone imagine ignoring the fact that cash dominates in most countries in the region? Grab took a different path: it adapted. Cash payments, localized interfaces, and services that catered to even the smallest user habits. It’s like trying to please every guest at a dinner party — some want more salt, some prefer sugar-free, and others need it spicy. Grab (Ticker: GRAB) understood this and, it seems, succeeded.

A Look at the Numbers

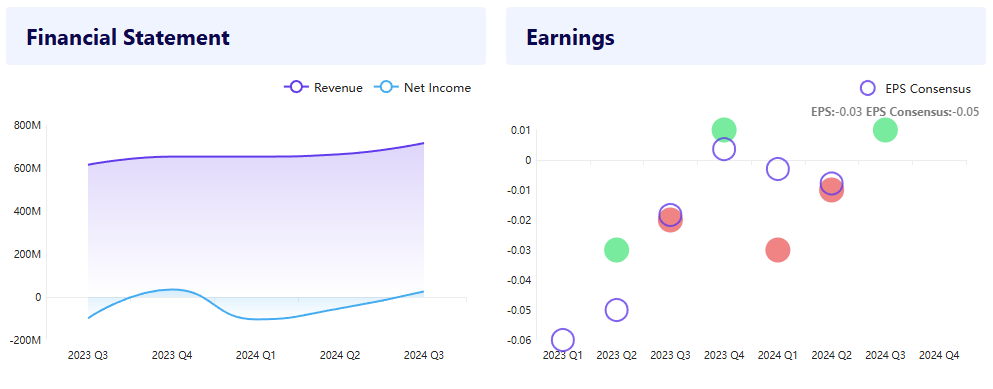

Let’s look at the facts. Third quarter of 2024: revenue — $716 million, a 17% increase compared to the previous year. Gross Merchandise Value (GMV) — $4.7 billion, up 15%. Adjusted EBITDA reached $90 million. For those unfamiliar, this is a record high for the company! And here’s the key point: $15 million in profit compared to a $99 million loss a year ago. That’s optimistic.

Now let’s compare this to Uber. Over the same period, Uber reported $9.6 billion in revenue, an 11% year-over-year increase. However, their adjusted EBITDA was $916 million, which is ten times that of Grab. Uber also reported $326 million in net profit, significantly more than Grab. But here’s the context: Uber operates globally, while Grab is focused on Southeast Asia.

Interestingly, Grab’s incentives in the third quarter totaled $462 million, or about 9.8% of GMV, while Uber spent about $1.2 billion on incentives, roughly 12.5% of their total revenue. This shows that Grab manages incentives more efficiently despite its smaller scale.

Personal Observations

How sustainable Grab’s business is? In the third quarter, the company repurchased its own shares worth $58.2 million. That’s a signal of confidence in its future. But here’s what worries me: the cost of incentives for customers and partners amounted to $462 million. That’s a huge sum. What will happen if they reduce these incentives? Will users leave?

Inspiring Stories

I recall a story from a friend in Bangkok. He told me how Grab literally saved him during the crisis. “When everything stopped, I became a Grab driver and then joined GrabFood. It helped me and my family survive.” Sounds inspiring, but it’s also a business solution that works. The question is, for how long?

Competition

Of course, Grab (Ticker: GRAB) isn’t the only player. Gojek, ShopeeFood, FoodPanda — all want a piece of the market. An interesting fact: Grab’s food delivery market share is currently 55%. That’s impressive, but can the company maintain its top position? The real question is: what will they do next to defend their position?

Uber also faces competition, but its market share in the U.S. remains consistently high — about 70% in rides and 24% in food delivery (via Uber Eats). However, on a global scale, they face similar challenges: local players often win thanks to better understanding of regional specifics.

Financial Stability

Let’s break down the numbers. Grab has $6.1 billion in cash on hand. Sounds impressive, right? But a $328 million debt hasn’t gone anywhere. Uber, on the other hand, has $6.9 billion in cash but over $9 billion in debt. This makes them more dependent on operational profits and continuous growth.

What’s Next?

Grab’s future looks both challenging and promising. On the one hand, the company continues to grow in one of the most dynamic regions in the world. Their strength lies in hyperlocalization and a deep understanding of Southeast Asia’s specifics. But can they scale their success beyond the region?

Grab’s financial services may become a key growth driver. For example, their loan portfolio grew 81% year-over-year, reaching $498 million. Moreover, customer deposits in their digital bank tripled, exceeding $1.1 billion. This demonstrates customer trust and potential for further growth in the fintech segment.

But there are challenges. Competition is intensifying, and the costs of user incentives remain significant. If the region’s economic situation deteriorates, it could impact their revenues. Additionally, Grab (Ticker: GRAB) will need to balance innovation and efficiency to stay competitive.

Alternative Scenarios

Two scenarios can be envisioned. In the optimistic one, Grab becomes not only a leader in Southeast Asia but also expands its ecosystem to other markets, possibly through partnerships or acquisitions. Their fintech business becomes the main profit source.

In a more pessimistic scenario, competitors like Gojek could capture market share, and users may leave due to reduced incentives. In this case, Grab will struggle to maintain its current position.

Conclusion

Grab may be on the brink of transforming into a large regional giant that will define the Southeast Asian market. However, their journey will be challenging. The appeal of investing in Grab (Ticker: GRAB) depends on the investment horizon. For short-term traders, it’s an opportunity to profit from technical growth and volatility. For long-term investors, Grab offers growth potential driven by fintech developments and expansion. However, it’s essential to remember the risks: competition, regulatory changes, and regional economic instability.

Investment Strategy

Short-Term Strategy

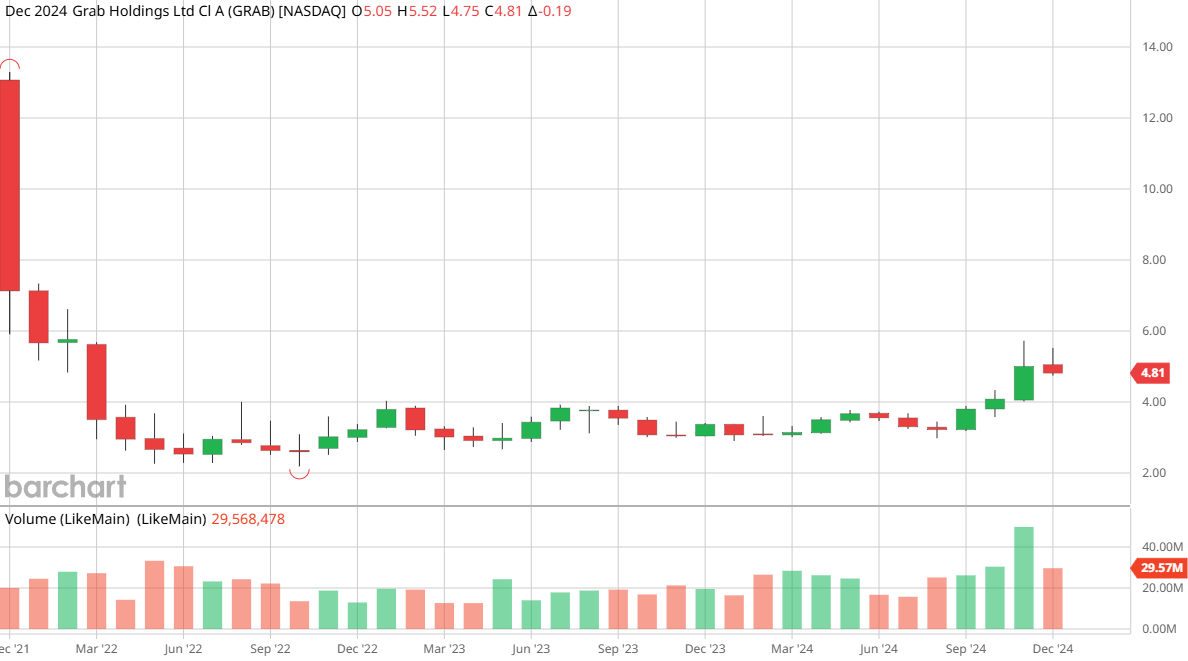

Current Price: $4.96

Target Price: $5.50–$5.75

Entry Point: Buy at $4.90 or below

Exit Point: Sell at $5.50 or above

Long-Term Strategy

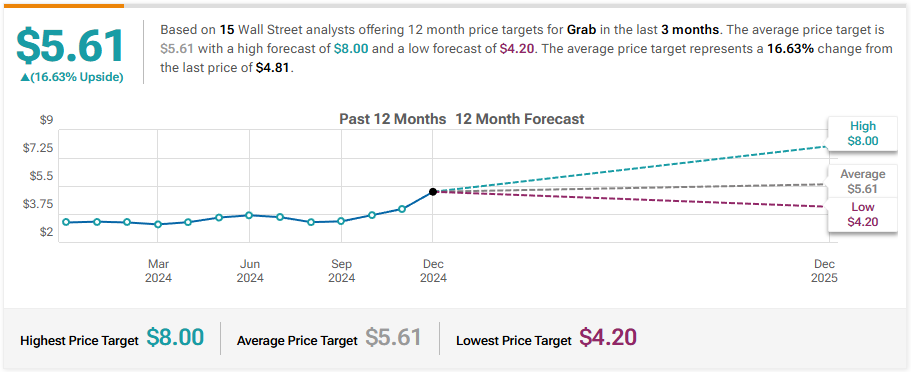

Target Price: $8.00 by 2026

Entry Point: Accumulate shares at $4.50–$5.00

Exit Point: Hold until $8.00 or significant market correction.

Investment Thesis

Grab’s growth trajectory is promising, with projected revenue growth of 17%–18% year-over-year. Recent profitability (net profit of $15 million in Q3 2024) demonstrates operational efficiency. The company maintains a strong cash position with over $6 billion in liquidity.

Risk Assessment

Market Competition: Intense competition from regional players could pressure margins.

Regulatory Risks: Regulatory changes could impact operations and profitability.

Execution Risks: Failure to scale technology or services could hinder growth.

Buy or Sell Signal

Currently, Grab shows a buy signal based on technical indicators. RSI is neutral (around 50), indicating no immediate overbought or oversold conditions. MACD is positive, suggesting bullish momentum.

Entry and Exit Strategies

Short-Term: Buy at $4.90; sell at $5.50.

Long-Term: Buy at $4.50–$5.00; hold until $8.00.

Good or Bad Investment?

Short-Term: Good investment — expected price growth based on recent performance.

Long-Term: Good investment — solid growth potential, but monitor competition and regulatory risks.