Market News 09 FEB

Weekly Summary and Key Events

Market Trends Overview The past week was challenging for investors: major indices were under pressure and ultimately closed in the red. The S&P 500 recorded a 0.4% decline, while the Nasdaq Composite lost 0.5% of its value. Volatility remained high amid geopolitical developments and new macroeconomic data.

Changes in Trade Tariffs and Their Impact The U.S. administration announced an increase in tariffs on imports from Canada, Mexico, and China. Specifically:

A 10% tariff was imposed on Canadian energy supplies.

Imports from China are subject to an additional 10% tariff.

China responded with similar measures, including increased tariffs on U.S. coal, agricultural machinery, and automobiles.

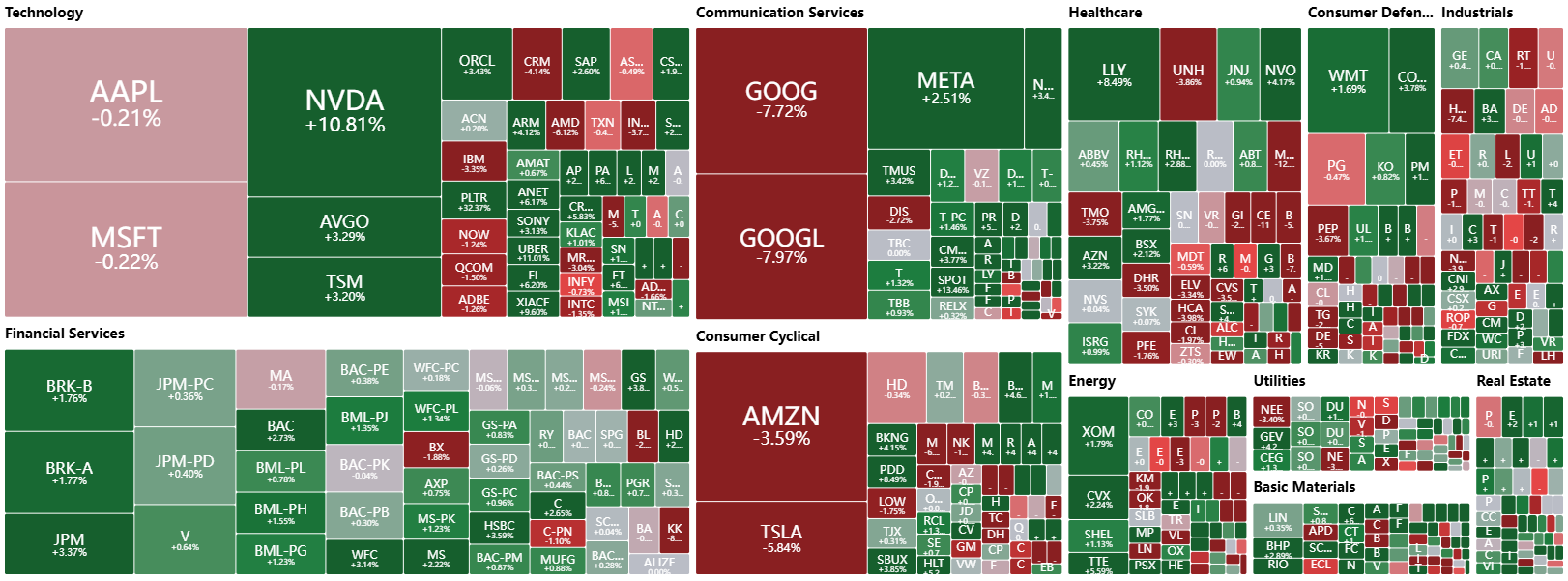

Additionally, China announced new export restrictions on strategically important resources such as tungsten and initiated an antitrust investigation against Google (GOOG), causing nervousness in the market.

Macroeconomic Indicators and Expectations Employment and inflation data also influenced market sentiment. Key reports include:

The number of job openings in the U.S. fell to 7.6 million from 8.1 million last month.

The average hourly wage increased by 0.5%, intensifying inflation expectations.

Business activity indices in the U.S., Europe, and China showed slowing growth.

The University of Michigan reported an increase in inflation expectations from 3.3% to 4.3%.

Amid these data, expectations for a Federal Reserve rate cut were revised: the probability of a rate decrease by June dropped from 64.6% to 52.8%.

Bond Yields and Corporate Earnings Treasury bond yields showed mixed dynamics:

The yield on 2-year bonds increased by 4 basis points to 4.28%.

The yield on 10-year bonds fell by 8 basis points to 4.49%.

Earnings reports from major companies influenced market sentiment:

Alphabet (GOOG) lost 9% after disappointing financial results.

Amazon (AMZN) declined by 3.6%.

Palantir (PLTR), Qualcomm (QCOM), Spotify (SPOT), and PepsiCo (PEP) reported mixed results.

Corporate Sector News Among the most discussed events:

The sale of TikTok's U.S. business is gaining momentum. Potential buyers include Microsoft (MSFT) and Oracle (ORCL).

Military startup Anduril plans to double its valuation to $28 billion through a new funding round.

Amazon (AMZN) fell by 4% following a weak forecast for the next quarter.

Roblox (RBLX) is under SEC investigation amid scandals related to child safety on the platform.

Centrus Energy (LEU) shares surged by 33% due to strong earnings and government contracts.

The past week demonstrated the stock market's vulnerability to changes in trade policy, macroeconomic risks, and corporate reports. In the coming weeks, investors will continue to monitor tariff negotiations, shifts in monetary policy, and new financial disclosures from major companies that could set the market tone for the months ahead.