Market News 12 FEB

Trade Wars, Inflation Risks, and Corporate Reports

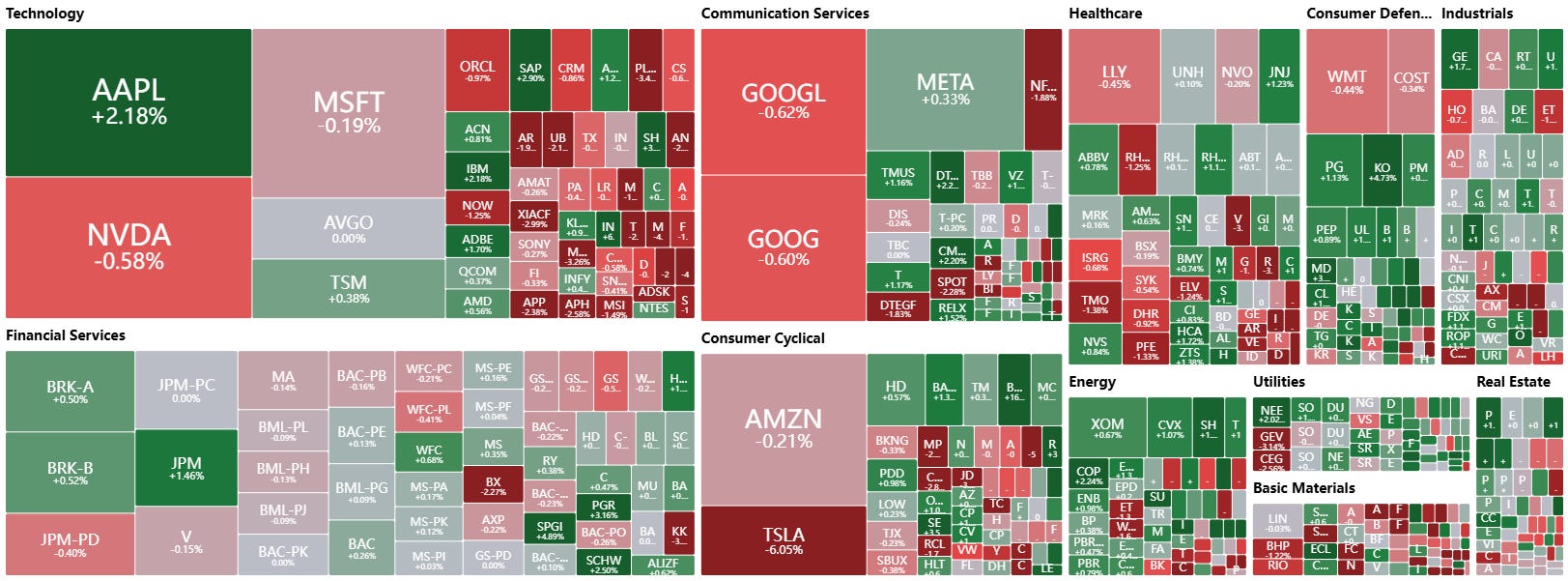

On Tuesday, U.S. stock indices showed mixed performance. The S&P 500 (SPX) (+0.03%) and Dow Jones Industrial Average (DOWI) (+0.28%) ended the day with slight gains, while the Nasdaq 100 (IUXX) (-0.29%) closed lower. The tech sector faced pressure due to new trade barriers and statements from Federal Reserve officials about maintaining tight monetary policy.

Trade Wars: A New Round of Confrontation

Markets reacted negatively to President Trump's announcement of a 25% tariff on steel and aluminum imports. This move prompted an immediate response from the European Union. European Commission President Ursula von der Leyen promised retaliatory measures, potentially escalating trade tensions between the U.S. and Europe.

Beyond the potential impact on exports, investors are concerned about inflationary risks that may rise due to increased metal prices. As a result, markets are pricing in a longer period of high interest rates.

The Fed: Rates Will Remain High

Additional pressure on the market came from comments by Fed Chair Jerome Powell and Cleveland Fed President Loretta Mester. They emphasized that there is currently no need to lower interest rates, as the economy remains resilient.

There is no urgent need to adjust monetary policy given the current inflation levels and strong macroeconomic indicators, Powell stated.

Markets responded to the Fed’s statements with a +3.8 basis point increase in the 10-year Treasury yield, adding to the pressure on stocks.

Corporate Reactions: From Tech to Traditional Giants

Super Micro Computer (SMCI) fell 3% in after-hours trading following preliminary Q2 results. Despite revenue growth of 54% (to $5.6–$5.7 billion), investors were disappointed by the company’s forecasts.

Tesla (TSLA) remained under scrutiny from analysts. Oppenheimer expressed concerns over increasing competition in the EV and autonomous driving sectors. Additionally, the market reacted negatively to Elon Musk’s investment in OpenAI, which was valued 38% lower than last year’s funding round.

Upstart Holdings (UPST) surged after posting strong quarterly results: revenue grew by 56.1%, and non-GAAP EPS came in at $0.26, beating analysts’ estimates.

Coca-Cola (KO) reported a 7% increase in EPS despite currency headwinds and franchise-related challenges. The company continues to expand its market share through innovation and pricing strategies.

Lyft (LYFT) reported a 27% increase in revenue to $1.6 billion, while adjusted EBITDA doubled to $112.8 million. However, the company's guidance for Q1 2025 was weaker than expected, leading to moderate stock corrections.

Market Winners: Intel, CRISPR, and DoorDash

Intel (INTC) was one of the top performers of the day, jumping 9% after a U.S. government official announced plans to expand AI chip production domestically. This move aligns with the White House’s strategy to maintain technological leadership and reduce reliance on foreign suppliers.

CRISPR Therapeutics (CRSP) also gained momentum following positive quarterly earnings and news of reimbursement agreements for its new sickle cell anemia therapy in the UK.

In the food delivery sector, DoorDash (DASH) posted strong results, with revenue up 25% to $2.9 billion and a 19% increase in orders. A record number of active users and an expanded selection of restaurants contributed to the company’s strong market position.

Awaiting New Market Drivers

Markets remain influenced by macroeconomic factors and corporate earnings. In the coming weeks, investors will closely watch the Fed’s statements, developments in trade conflicts, and further movements in bond yields.

Tech stocks continue to be under pressure due to the prospect of tighter monetary policy, while industrial and traditional sectors, such as energy and consumer goods, are showing relative stability. In the near term, key market catalysts will be upcoming economic data and policy decisions that could shift the balance of power on Wall Street.