Market Overview Last Week

Major Developments and Their Market Influence

Donald J. Trump took office as the 47th President of the United States this week, coinciding with the celebration of Martin Luther King Jr. Day. The trading week began on Tuesday after the holiday weekend, and markets quickly regained momentum thanks to the President's announcements of emergency energy measures and several executive orders that did not include tariffs on China. However, the possibility of introducing 25% tariffs on Canada and Mexico starting February 1 was discussed.

Key Initiatives and Market Impact

Excluding China from the list of countries facing strict tariffs contributed to market growth, further supported by a $500 billion AI initiative involving OpenAI, Softbank, and Oracle. On Wednesday, the positive sentiment was reinforced by Netflix's strong earnings report and the success of Dow companies like Procter & Gamble and Travelers. The S&P 500 index reached a new all-time high and ended the week on a strong note.

Economic Policy and Foreign Initiatives

In a virtual speech at the World Economic Forum in Davos, Trump emphasized his pressure on OPEC and Saudi Arabia to lower oil prices. The President also urged NATO countries to increase defense spending to 5% of GDP. Additionally, he highlighted the benefits of tax incentives for foreign companies manufacturing products in the U.S. and criticized the Federal Reserve Chair ahead of the FOMC meeting, hinting at the need for rate cuts.

Upcoming Focus

Next week, attention will turn to the FOMC meeting and earnings reports from major tech companies, including Apple, Microsoft, Meta, Amazon, and Tesla. While no rate cuts are expected, the President's comments have added intrigue to the upcoming events.

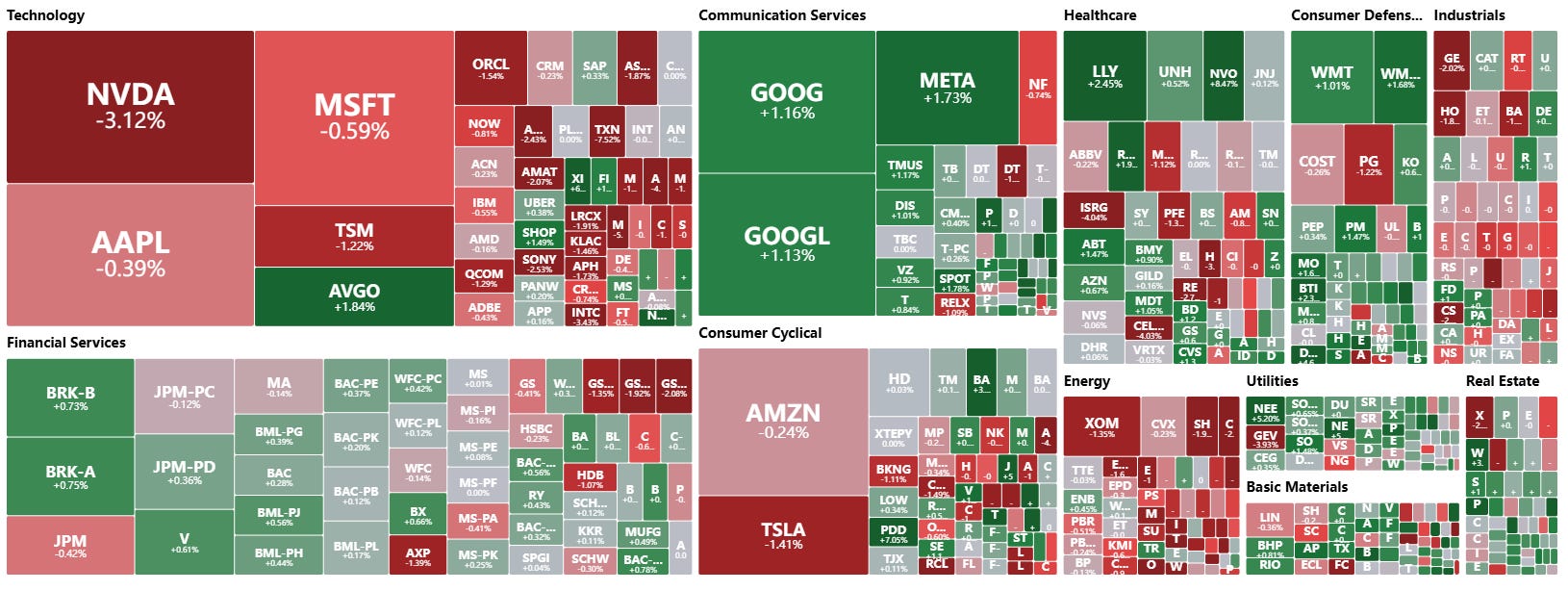

Market Dynamics and Sector Performance

For the week, major indexes posted gains ranging from 1.1% to 2.2%. The communication services sector led the way with a 4.0% increase, while the energy sector declined by 2.9% due to concerns about supply and demand imbalances. The Treasury market remained stable, while the U.S. dollar weakened by 1.7%, which supported equities.

Daily Trading Highlights

Tuesday: Markets reacted positively to the absence of tariffs on China. The performance of 3M and Oracle's participation in the AI initiative also played a key role.

Wednesday: The S&P 500 hit a new record high, boosted by Netflix's impressive subscriber growth.

Thursday: Gains were driven by stocks like NVIDIA, Amazon, and Microsoft.

Friday: The week ended on a cautious note, with markets reacting to weak consumer sentiment and forecasts from companies like Texas Instruments and Boeing.

Corporate News and Investor Strategies

Chris Davis made several transactions, including reducing his stake in VTRS and increasing investments in MGM. Key company updates included:

MicroStrategy may face a 15% tax on unrealized gains, impacting its financial results.

Meta Platforms announced significant AI investments, including building a powerful data center.

Palantir shares continued to rise, supported by positive analyst forecasts.

Novo Nordisk faced criticism over misrepresentation of healthcare payments.

Texas Instruments came under pressure due to weak first-quarter projections.

Market in the Context of Global Events

Amid global uncertainty, investor focus remains on Trump's policies, the AI initiative, and economic forecasts. These factors will be pivotal in shaping market dynamics in the coming weeks.