Mattel: From Dolls to the Big Screen — The Empire That Grew Up With Us

Barbie, Hot Wheels, and Fisher-Price — childhood brands now leading the game in innovation, content, and major investments.

Mattel, Inc. (NASDAQ: MAT) is not just a toy manufacturer. Barbie, Hot Wheels, Fisher-Price—these brands have become a part of childhood for millions. But have you ever thought about the massive machinery behind it all? When i was a kid, I used to think that the people making dolls in factories were related to Willy Wonka or Santa Claus. At seven, the idea that a mouse with legs doesn’t sit on Disney’s board of directors might also seem incredible.

Read this first:

Financial report Mattel, Inc

Over decades, the company has transformed into a multifaceted giant, not only producing toys but also venturing into content creation, gaming, and licensing. They’ve even stepped into the world of cinema—the success of the Barbie movie is a testament to that. Quite a controversial movie, if you ask me. The company’s headquarters is located in sunny California, El Segundo. As is our tradition, let’s start with the numbers.

Key Numbers to Know

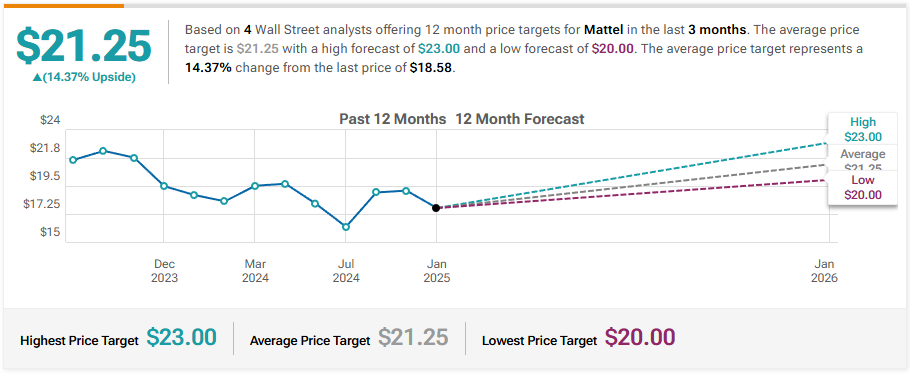

Current Price: $18.52

Price-to-Earnings (P/E) Ratio: 11.8

52-Week High/Low: $20.60 / $15.87

Forward Earnings Per Share (EPS): $1.59

PEG (Price/Earnings-to-Growth): 9.29—something seems to be slowing down this toy empire.

Personal Take: What to Do with This?

At first glance, Mattel looks cheap. A P/E ratio of just 11.8 suggests it’s a “buy, hold, and smile” stock. But the PEG of 9.29 is concerning. Such a high number seems to say, “Don’t expect miracles here; growth will be slow, very slow.”

The company is cutting costs, diversifying revenue streams, and leaning into licensing and films, which have long been the norm for corporations.

What’s Really Going On?

At the moment, Mattel’s stock is trading at $18.52, roughly in the middle of its annual range. On the one hand, the low P/E ratio is good news. On the other, the high PEG suggests there aren’t many growth drivers.

Their new projects in entertainment could change the game if the company maintains efficiency.

Revenue

For the nine months ending September 30, 2024, Mattel earned $3.73 billion. Yes, it’s slightly less than the $3.82 billion in the same period last year. Is this catastrophic? Hardly. The main reasons are fluctuations in demand and product updates. Key categories like Barbie and Hot Wheels are still holding strong.

Balance Sheet

The company holds $724 million in cash—a nice “cushion,” especially with a current ratio of 2.45. Debt remains stable at $2.33 billion. For a company actively investing, this looks solid.

Cash Flow

This area raises some questions. Operating cash flow went negative at -$62 million. Why? Simply put, they increased accounts receivable and built up inventory. On one hand, it feels like a “growth strategy,” but on the other, it’s crucial not to get stuck in this position.

Interestingly, investments are also active: $152 million was spent on property and equipment, and $268 million went to share buybacks. This move is essentially a goodwill gesture for shareholders. However, it always raises the question: was the money spent in the right place? Share buybacks often signal stagnation.

Profitability

Gross profit for the same period increased to $1.90 billion, a decent improvement compared to $1.79 billion a year earlier. The gross margin is about 50.9%. This, no doubt, shows they’re keeping expenses in check. But net income surprised even more: $401 million compared to just $67 million last year. That’s what operational efficiency can do!

Growth Areas

Now for the exciting part. Mattel clearly knows where to look for growth:

Expanding product and license lines: Toys based on popular franchises are “in vogue.”

Strong brand: The success of the Barbie movie proves this.

Innovation: Digital games and virtual platforms are steps into the future. Who knows? Kids might soon “play” Barbie in the metaverse.

Insiders are Very Positive Buying More Shares Than They Are Selling In Mattel

In the last 100 trades there were 1.98 million shares bought and 552.59 thousand shares sold. The last trade was made 120 days ago by Kreiz Ynon who bough 787.4 thousand shares. The large amount of stocks bought compared to stocks sold indicate that the insiders believe there is a potential good upside. In some cases larger purchases can be explained by due date for stock options.

Risks: What If Things Go Wrong?

Toys are essentially “discretionary” items. When the economy slows, so do sales. Additionally:

Economic Dependency: Toys aren’t bread; during tough times, they’re the first to go.

Leadership: The recent announcement of CFO Anthony DiSilvestro’s departure raises questions. Who will replace him, and what will change?

Short-Term Strategy: Playing the Range

Buy: Around $18.00—an important support level.

Sell: Near $19.50–$20.00, if the stock approaches resistance.

Stop-Loss: At $17.50 to limit downside risk.

Long-Term Strategy: Betting on Patience

Investors with a 3–5 year horizon might find Mattel attractive. Their diversification, including movies and licensing, could provide steady income. If things go well, a target of $22.00–$24.00 seems realistic.

My personal Opinion

In my view, Mattel is a company with immense potential. They’ve figured out how to improve profitability, their brands need no introduction (even adults know Barbie), and their investments in new technologies look promising.

However, if the company continues experimenting and innovating—whether through films, digital platforms, or unique products—they could become a long-term asset for a portfolio. Still, caution is necessary: liquidity and inventory management are two aspects that could play tricks.

I’ll be adding them to my portfolio for the year. Let’s not forget to monitor how they handle innovation and margins.