Novo Nordisk: Growth, Prospects, and Challenges for a Pharmaceutical Leader

How the Company Maintains Its Position in Diabetes and Obesity Treatment and the Risks It Faces

When talking about leaders in diabetes and obesity treatment, the first name that comes to mind is Novo Nordisk (NVO). Founded in 1923 in Denmark, the company has come a long way from an insulin producer to a global leader in developing innovative drugs for diabetes, obesity, and rare blood disorders. Today, the brand is associated with blockbuster drugs such as Ozempic, Wegovy, and Rybelsus—names that increasingly appear not only in medical reports but also on the pages of business publications.

Read this first:

Financial report Novo Nordisk

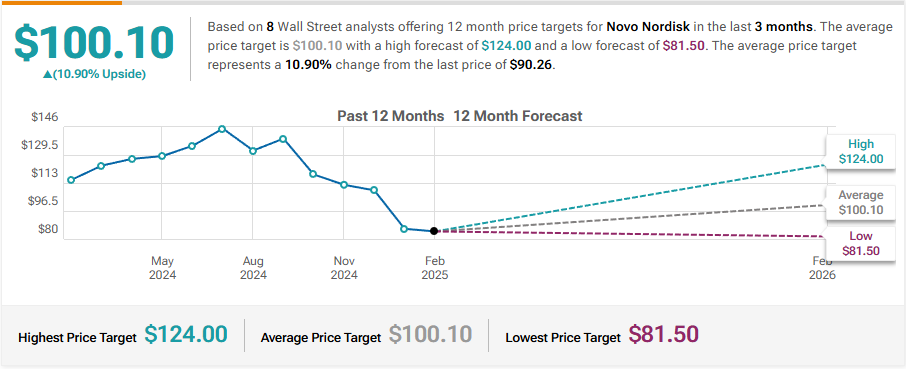

The market currently favors pharma, but selectively. After rapid growth, Novo Nordisk shares have pulled back slightly, raising a critical question: is this a buying opportunity or a sign of trouble?

Financial Performance: Where is the Money Going?

2024 has been a successful year for Novo Nordisk. Revenue surged to DKK 290.4 billion, marking a 25% increase compared to the previous year. The primary growth driver? Obesity drugs, with sales soaring by 57%. As people become increasingly aware of weight-related issues, pharmaceutical companies are converting this awareness into billions. Meanwhile, the rare disease segment exhibited a more modest but stable growth of 9%.

At the same time, the company maintains phenomenal profitability:

Gross margin – 84.7%

Operating margin – 44.2%

Net profit – DKK 101 billion (+21% YoY)

Earnings per share (EPS) – DKK 22.67 (+21%)

These numbers speak for themselves: the business is highly profitable and consistently generates earnings. However, there’s a catch—free cash flow (FCF) turned negative at -DKK 14.7 billion. Why? The key reason is a major asset acquisition from Catalent. Investors expect returns, but for now, it's just an expense.

Balance Sheet: Cash is There, But How Will It Be Used?

The company is not afraid to spend, yet its balance sheet remains strong. Total assets have risen to DKK 465.8 billion (+48%), while equity increased by 35% to DKK 143.5 billion. Particularly impressive is the return on invested capital (ROIC) of 63.9%—a staggering figure that many companies can only dream of achieving.

Novo Nordisk hasn’t forgotten about investors: dividends have increased by 21% to DKK 11.4 per share, while share buybacks, despite being reduced by 33% from 2023, remain substantial at DKK 20.2 billion.

Key Growth Drivers: Where is the Company Headed?

If anyone thought the success of Wegovy and Ozempic was the peak for Novo Nordisk, the company is eager to prove otherwise. Several promising developments are on the horizon:

CagriSema and Amycretin – potential breakthroughs in obesity treatment.

Ziltivekimab – a leading candidate for combating cardiovascular diseases.

Mim8 – a new hope for hemophilia A patients.

Artificial intelligence in research – sounds like hype, but in reality, AI is already accelerating drug development.

Risks: What Could Go Wrong?

Setting aside short-term fluctuations, Novo Nordisk appears to be a strong player for the next 5+ years. Why? Because obesity and diabetes are not just trends—they are growing global health concerns. The number of overweight individuals worldwide continues to rise, meaning demand for drugs like Wegovy is likely to increase.

Additionally, governments in various countries are discussing subsidizing obesity treatment (in the U.S., there’s already an active debate about partially covering such drugs under insurance). In this context, Novo Nordisk's business model looks solid.

But risks remain:

Overconcentration in one area – More than 80% of the company’s profits come from GLP-1 drugs (Ozempic, Wegovy). What if competitors like Eli Lilly or Pfizer introduce something better?

Regulatory risks – U.S. authorities are already discussing drug price caps. For a company that generates a significant portion of its revenue from the American market, this could be a challenge.

Rising R&D and production costs – Capital expenditures (CapEx) in 2024 reached DKK 47.2 billion—a massive amount. The key question is how efficiently these funds will be utilized.

Is It Worth Investing?

Novo Nordisk is a company worth following closely. It generates solid profits, outpaces competitors, and sets the rules in its industry. However, important questions remain: how long will the obesity market grow at this pace? And can the company diversify its revenue streams if something goes wrong with GLP-1 therapy?

Pros:

High profitability and revenue growth.

Leadership in innovative drug development.

Dividends and share buybacks.

Cons:

Intense competition.

Regulatory risks.

Massive capital expenditures.

If you are considering NVO shares for the long term, they are worth buying, especially during pullbacks. However, as with any investment decision, it's essential to stay cautious and understand what you're betting on.