Payoneer: A Fintech Growth Story with Strong Investment Potential

Analyzing Payoneer’s Financial Performance, Profitability Trends, and Key Risks for Investors

Payoneer Global Inc. (NASDAQ: PAYO) is one of the largest players in the cross-border payments market for small and medium-sized businesses (SMBs). The company provides entrepreneurs worldwide with access to international financial infrastructure, reducing barriers to entry into the global economy.

Read this first: Financial report Payoneer Global Inc.

But is Payoneer a promising investment? Should it be considered a long-term asset in a portfolio? Let’s analyze fresh financial indicators to find out.

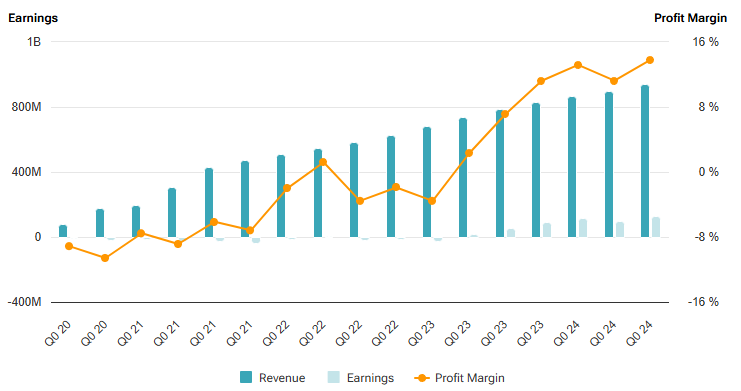

Revenue and Growth Dynamics: Is Payoneer Outpacing Competitors?

Payoneer’s financial results demonstrate steady growth:

Revenue for 2024 reached $977.7 million, an 18% increase from $831.1 million in 2023.

In 2022, the company earned $627.6 million, indicating over 55% growth in two years.

The total transaction volume on the platform increased by 21%, reaching $80.1 billion.

Revenue growth was driven by an expanding client base and monetization of new services.

SMB segments showed significant growth:

Marketplace sellers – by $66.3 million,

B2B payments – by $47.0 million,

DTC (Direct-to-Consumer) sellers – by $13.7 million.

Interest income on customer balances contributed an additional $26.2 million, supported by rising interest rates and growing customer balances.

What Does This Mean for Investors?

Payoneer’s growth is outpacing many fintech companies, such as PayPal (+7% annual growth) and even Wise (+24%). Notably, the company maintains sustained double-digit growth despite strong competition. If this trend continues, Payoneer has every chance of surpassing $1 billion in revenue in 2025.

Profitability: Payoneer Moves into Profit

Payoneer’s profitability has significantly improved over the past two years. Net income for 2024 – $121.2 million (a 30% increase from $93.3 million in 2023). In 2022, the company recorded a net loss of $12 million, highlighting substantial progress. Net margin increased from 11% to 12%, while operating margin rose to 15%. Operating profit reached $149 million (compared to $103.6 million a year earlier). Gross margin remains at 84–85%, higher than many competitors. Interest income ($257 million, or 26% of revenue) significantly boosted profitability. Operating expenses (sales, marketing, R&D) grew by 14%, but at a slower rate than revenue growth, enhancing profitability.

How Does Payoneer Compare to Competitors?

Despite the improvement, Payoneer still lags behind PayPal (17% net margin) and Wise (21%). However, the trend suggests further profitability growth, making the company an attractive prospect for investors.

Cash Flows: Where Does the Money Go?

Payoneer’s operational cash flow remains strong and growing:

Net cash flow from operating activities in 2024 – $176.9 million (up from $159.5 million in 2023 and $84 million in 2022).

Major investment expenses: -$1.961 billion (compared to -$44 million in 2023).

The main reason for this jump – investments in U.S. Treasury bonds ($1.167 billion) and term deposits ($600 million) from customer funds.

Acquisition of Skuad for $48.2 million added new B2B hiring capabilities.

Share buybacks amounted to $136.8 million, signaling management's confidence in the company’s undervaluation.

Total free cash balance – $497 million, providing the company with financial flexibility.

Balance Sheet and Capital

Payoneer’s balance sheet highlights its financial stability:

Total assets at the end of 2024 – $7.93 billion (compared to $7.28 billion in 2023).

$6.964 billion of these are customer funds, held in banks and investments.

Net company liquidity – $497.5 million.

Payoneer has minimal liabilities: no debt, and accounts payable total just $37.3 million.

Shareholder equity grew to $724.8 million (up 9% year-over-year).

Payoneer’s financial stability surpasses some fintech competitors, especially given its lack of debt burden.

Risks and Challenges

1. Competition

Payoneer faces intense competition:

PayPal leads with $31.8 billion in revenue (32 times Payoneer’s size).

Wise is growing at +24% but is less diversified.

Competitors may undercut fees, pressuring margins.

2. Regulation

Payoneer operates in a highly regulated financial sector:

Licenses in the U.S., EU, Australia, Hong Kong, and India.

Potential new regulatory restrictions could complicate operations.

Possible investigations (though none are currently pending).

3. Dependence on Major Clients

23% of revenue comes from Amazon-related clients.

If Amazon or other marketplaces change their policies, it could negatively impact the business.

4. Financial Risks

Rising interest rates generated $257 million in revenue for Payoneer in 2024, but what happens if rates start declining?

Currency fluctuations could affect financial results.

Conclusion: Is Payoneer a Good Investment?

At present, Payoneer is a fast-growing fintech with strong positioning in the B2B payments sector. Key advantages:

Double-digit revenue growth.

Increasing profitability.

No debt.

Diversified revenue streams (fees + interest income).

Global infrastructure and licenses.

However, risks remain:

Intense competition.

Regulatory threats.

Potential changes in partnerships with key clients.

Payoneer is a promising investment for those who believe in the growth of global payments and B2B fintech. If the company continues its double-digit growth and improves profitability, its stock could see substantial appreciation. For long-term investors willing to accept some risks, Payoneer could be a strong addition to a diversified portfolio.