Roivant Sciences – The Future of Biotech or a Risky Gamble?

Billions in R&D, an unconventional business model, and high-risk venture capitalism in pharma.

How often have you come across biotech companies that promise a revolution but end up as just another statistic of failures? Roivant Sciences Ltd. (NASDAQ: ROIV) is one such player, but perhaps not a typical one. They have an unconventional approach: instead of a single company, they operate an entire network of subsidiaries ("Vants"), each developing a specific drug. It resembles venture capitalism in pharma—if one project fails, others might keep the business afloat.

In theory, it sounds promising, but in practice, it doesn’t always work. So the question remains: Is Roivant the next biotech giant or just a clever marketing ploy?

Read this first:

Financial report Roivant Sciences

Where Does the Stock Stand Now?

• 52-Week Range: $13.06 — $9.69

• P/E Ratio: 2.05 (but this figure is misleading—we’ll analyze it later)

• EPS Growth Rate: -121.48% (a significant decline)

• Dividends: Not paying, and given their strategy, unlikely to start.

A P/E of 2.05 makes the company look cheap. But let’s not jump to conclusions. This low ratio is merely the result of one-time profits. The real picture is far less optimistic: forward EPS is already negative (-$1.19), and the PEG ratio is also in the red (-0.02). That’s a warning sign.

Revenue: Growth, but with Caveats

For the six months ending September 30, 2024, the company generated $12.47 million in net revenue—a clear improvement from $8.13 million a year earlier. At first glance, this seems like an excellent result!

But let’s take a closer look at where this money came from. The primary sources are licensing and milestone payments—essentially, these are not stable revenue streams but rather one-time transactions. Of course, money is money, but the real question is: where’s the sustainability?

Profitability: Still in the Red, but Losses Are Shrinking

Yes, the net loss remains massive—$222.43 million for the past six months. However, compared to last year’s $658.96 million, it seems like things are moving in the right direction.

The difference is indeed significant, but let’s not get ahead of ourselves. The company’s main expenses—R&D and administrative costs—are still consuming all of its revenue. In other words, Roivant isn’t making money yet; it’s burning cash, betting on the future.

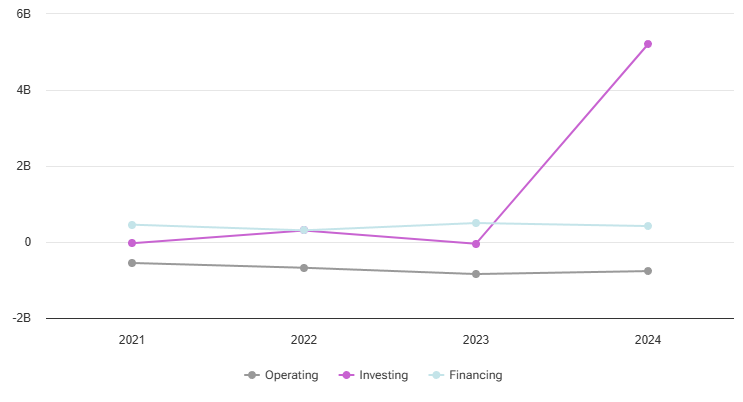

Cash Flows: Where Is the Cash Going?

Operating Cash Flow: -$459.63 million → The business is not only failing to generate cash but is actively burning it. Investing Cash Flow: -$3.29 billion → A massive outflow, primarily due to spending on marketable securities. Share Buybacks: -$769.69 million → Adding to the net cash outflow. Why spend so much money when the business is still unprofitable? That’s the big question.

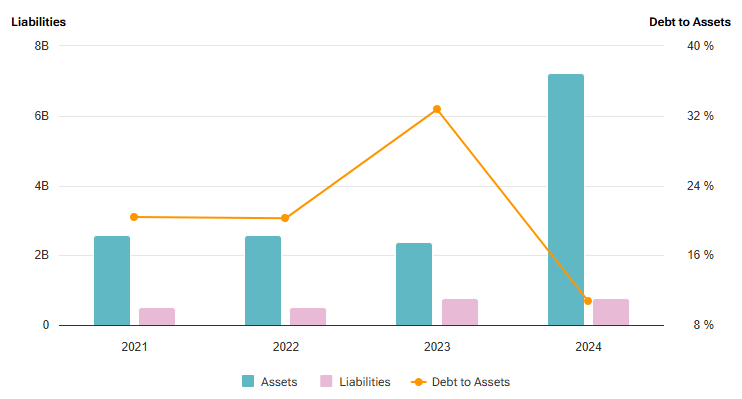

Balance Sheet: A Stability Cushion

Roivant has $6.2 billion in total assets, including $5.4 billion in cash and equivalents. With only $626 million in total liabilities, it has a light debt load.

This indicates that for the time being, bankruptcy is not a problem. The crucial query, though, is how this money will be put to use. Although having such a sizable cash reserve is comforting, investors are eager to see it used.

Risks & Difficulties: The Real World Isn't That Easy

Expensive R&D: Biotech is a costly field, and not all projects result in profitable products.

Regulatory Obstacles: The FDA is a powerful gatekeeper that has the authority to approve a medication or reject multimillion-dollar expenditures. It is more than just three letters.

Is it profitable? When? The market dislikes ambiguity, and it is unclear when the company will become profitable.

Investor Sentiment: If news disappoints, the stock could take a hit.

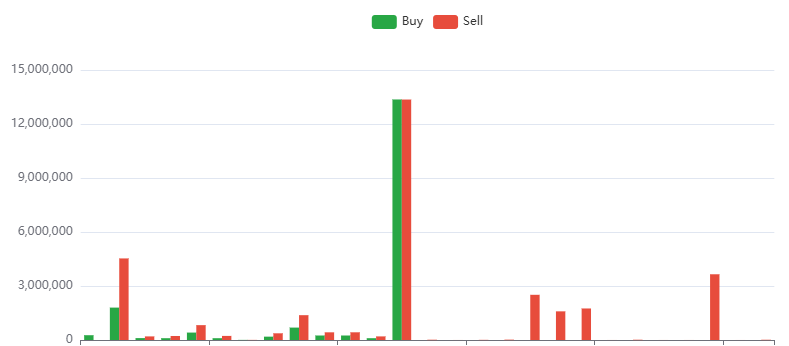

Insiders are Negative Selling More Shares Than They Are Buying In Roivant Sciences Ltd.

In the last 100 trades there were 17.63 million shares bought and 31.81 million shares sold. The last trade was made 8 days ago by Epperly Melissa B, who bough 1.67 thousand shares. In general the insiders are selling more stocks than they buy. There can be a variety of reasons for this, but in general it can be considered as a negative signal.

Short-Term Outlook: Is a Drop Coming?

Technical analysis suggests that the market is uncertain about the stock right now.

RSI: 40.93 → Not yet in oversold territory but close to a strong support level around $10.89.

Potential Rebound? There could be a small bounce, but confidence in it is low.

If you like stocks that offer a "catching a falling knife" opportunity, Roivant is one of them—just don’t try to catch it with bare hands.

Growth Areas: Where Is the Potential for Revenue?

As a strategic move, Roivant is actively selling non-core assets, including Telavant, to raise money and concentrate on important goods.

Investments in Innovation → The company is betting on cutting-edge biotech developments. Partnerships & Deals → Collaborations like Dermavant and Telavant could open new revenue streams.

However, it’s still unclear which of these bets will generate significant profits.

Long-Term Bet: Risky or Justified?

The most intriguing aspect is Roivant’s future potential. The company has strong drug candidates, such as IMVT-1402 and brepocitinib. If trials go smoothly, the stock could soar. But there’s a catch. The failure of namilumab serves as a reminder that success in biotech is never guaranteed.

High Expenses: The company’s negative free cash flow of $781 million raises concerns about how long it can sustain its R&D spending. Regulatory Risks: In biotech, everything hinges on FDA approval. Bad news can send the stock crashing within hours.

Valuation: If you’re willing to wait 2–3 years, a price below $10.50 could be a reasonable entry point.

Upside potential: $17–$20, but only if clinical trials succeed.

Is It Worth the Gamble?

Roivant is a classic high-risk/high-reward stock. If you have steel nerves and a long-term perspective, this could be a long game worth playing. The company’s strong cash reserves provide time for development, but profitability remains a big question mark.

What Could Drive a Big Rally? Successful clinical trials in 2025 could shift market perception and push the stock to new highs.

What Could Sink It? High spending, weak financials, and regulatory risks.

Should You Invest?

In a one-year horizon, this stock should be only a small part of a diversified portfolio. If positive news about clinical trials or new partnerships emerges, expect a surge. Without that, simply holding and waiting may not be the best strategy.

Buy or Not?

Only if you’re prepared for high volatility and fully understand the risks. This isn’t a blue-chip stock—it’s more like a lottery ticket where the potential payout might be worth the wait.