SelectQuote (SLQT): Soaring on Pharma.

The pharmacy business is pushing the stock up, but does it have enough staying power?

SelectQuote Inc. (SLQT): Growth in the Pharmacy Business or Temporary Success?

Looking at the SelectQuote (SLQT) chart, I ask myself: what is happening with this company? Not long ago, its stock was hovering near the bottom, and now it’s experiencing significant growth.

Read this first:

Financial report SelectQuote Inc.

What Does SelectQuote Do?

SelectQuote is not an insurance company but rather an intermediary between clients and insurers. Its business revolves around selling health insurance (including Medicare Advantage), life insurance, auto insurance, and homeowners insurance. They make money from commissions, earning a percentage from insurance companies.

The insurance brokerage market is highly competitive, where customers demand low prices, and regulators require transparency. SelectQuote found a loophole: the pharmaceutical segment. Their prescription drug division, SelectRx, is growing at an explosive rate. But how sustainable is this growth?

Numbers, Numbers, Numbers: A Surge or a Bubble?

Revenue

Over the past six months (as of December 31, 2024), the company reported a 21% revenue increase to $773.3 million. Great news. Let’s dig deeper:

Commissions and other services – $440.4 million (+1%)

Pharmaceutical business (SelectRx) – $332.9 million (+64%)

Almost all the growth came from prescription drug sales, while the core business—insurance commissions—remains stagnant.

Profitability

SelectQuote managed to turn a profit, but it still looks shaky:

Operating income: $58.9 million (vs. $32.9 million a year earlier)

Net income: $8.7 million (last year, there was a $11.7 million loss)

The company is making money, but how? Primarily by cutting marketing expenses (advertising costs were reduced by $17.9 million). A good sign, but the debt burden remains enormous. We all know how marketing budgets can strain a company’s finances.

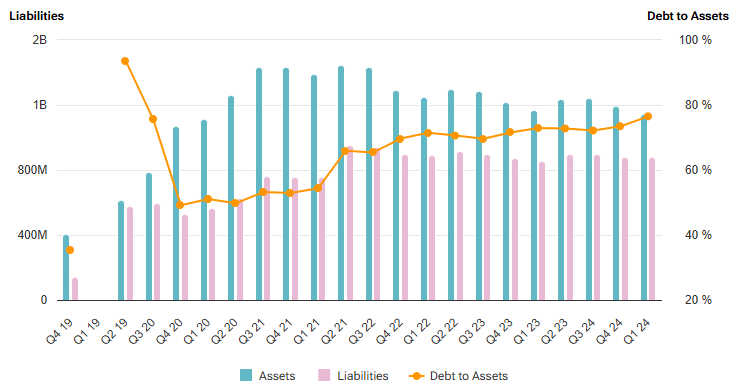

Debt and Cash

Here, the picture is more concerning:

Total debt – $711.9 million

Cash on hand – $12.1 million (was $42.7 million in June 2024)

Operating cash flow – negative $45.3 million

In other words, the company is still spending more than it earns.

What’s Driving SLQT Up?

SelectRx pharmacy business – 64% revenue growth! Customers buy prescription drugs through SelectQuote, creating a "subscription effect" and long-term cash flow.

Lower advertising costs – the company has learned to acquire customers more cheaply.

Medicare Advantage growth – the number of sold policies increased by 5%.

But there are serious risks as well.

Risks and Pitfalls

Massive debt – A $711.9 million debt weighs heavily on the company. Paying it off without additional funding will be difficult. Recently, they secured $350 million in additional financing from funds managed by Bain Capital, Morgan Stanley Private Credit, and Newlight Partners.

Reliance on commissions – Insurance commissions are not received immediately but are spread over years, leading to cash flow gaps.

Lawsuits – The company is facing securities-related lawsuits. If they lose, the financial consequences could be severe.

High competition – SelectQuote competes with giants like eHealth and GoHealth for customers.

Is It Worth Investing?

SelectQuote is definitely not for conservative investors. Its stock could easily double if SelectRx continues to grow and the company successfully restructures its debt. But if growth slows or new financial problems arise, a crash is inevitable.

If considering a buy, it’s better to wait for next quarter’s earnings reports. Will the company stabilize cash flow? Will the pharmaceutical segment continue to grow at the same pace?

At this stage, SLQT is pure speculation – high risk, high potential reward. Only if you know your risk tolerance and clearly define under what conditions you will take your invested money and run away in case of a bad situation. Are you ready for that kind of gamble?