Teva Pharmaceutical: A Pharma Giant on Thin Ice

Can This Debt-Laden Titan Turn Its Fortunes Around?

Teva Pharmaceutical (Ticker: TEVA) Industries is the very same pharmaceutical giant that started in Israel and now sets the rules in the global generics market. Yes, the company also has innovative drugs like Austedo for Huntington’s disease and Ajovy, which helps prevent migraines.

Read this first:

Financial report Teva Pharmaceutical

But let’s be honest—few people think about the challenges behind these achievements: a massive debt load, ongoing lawsuits, and financial instability. Yet, institutional funds continue to invest in it.

Let’s Look at the Numbers:

Current Price: $21.67

P/E Ratio: -25.49 (Yes, the losses are massive.)

52-Week High: $22.80, and the 52-Week Low? Just $11.48.

Forward EPS: $2.77

Where to Start Analyzing?

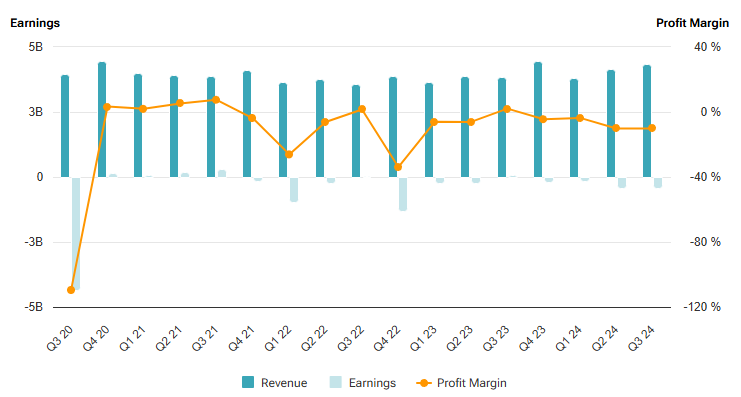

Revenue

Q3 2024 revenue reached $4.33 billion. At first glance, this number is impressive, especially compared to $3.85 billion in the same period last year—a 12.5% increase. But let’s dig deeper: where did this growth come from?

The U.S. market contributed $2.23 billion, followed by Europe with $1.26 billion, and international markets added $613 million. The contribution of new products is also a key factor. But the big question is: how long can this growth pace be sustained?

Profitability

Gross margin at 49.7% looks stable, but net profit leaves much to be desired. The loss for Q3 amounted to $390 million, while for the first nine months of 2024, it reached a staggering $1.68 billion. This contrasts with last year’s profit of $77 million for the same quarter. Why such changes? The main culprits are legal expenses ($450 million) and goodwill write-offs. Imagine it like a deflated balloon: it seemed to have volume, and then—pfft.

Cash Flow

Operating cash flow for the first nine months increased to $672 million, which might seem encouraging. However, it's too early to celebrate: investment cash flow is positive at $590 million, mainly due to the securitization of accounts receivable. In other words, the company has optimized its processes rather than attracted new funds. Financial cash flow, on the other hand, ended up negative at $1.1 billion due to debt repayments and dividend payments.

Balance Sheet

The company appears quite large, with assets totaling $41.76 billion. However, $16.12 billion of that is goodwill, which has already started to be written off (down by $1 billion). Cash on hand amounts to $3.32 billion, but with total debt nearing $19 billion, that’s just a drop in the ocean. The key question here is: can they handle such a debt burden, especially in an environment of high interest rates?

Growth Areas

There are promising areas of growth, such as biosimilars—recent agreements with mAbxience and Alvotech highlight this potential. Innovative drugs are also drawing attention, particularly in oncology and neurology. The approval of new products like SIMLANDI® (a Humira® biosimilar) and SELARSDI™ (a Stelara® biosimilar) is a positive sign. But will this be enough to offset the losses?

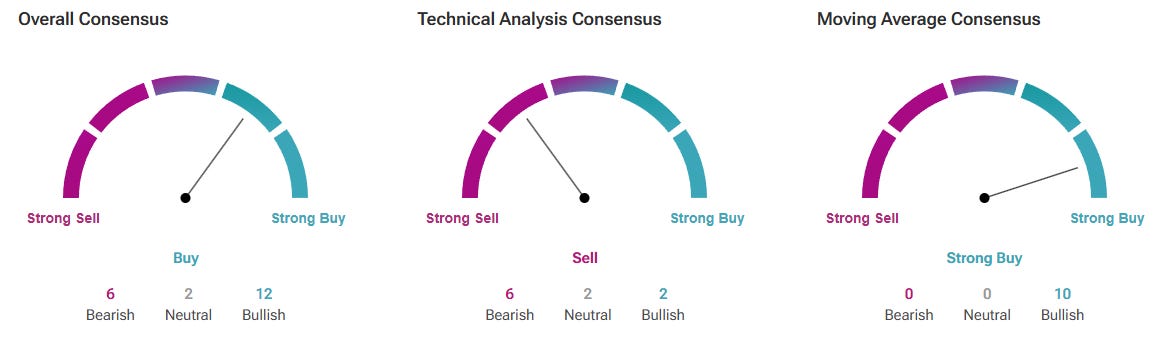

It seems the stock is treading on thin ice. For instance, revenue growth rates are off the charts… in the wrong direction: -425.88%! Is it difficult to call this a catastrophe?

Short-Term Strategy: Not for the Faint-Hearted

If you still want to play this volatility, stick to the $21.00–$21.50 range for entry. Why? This is the level where the price has stabilized in recent days (around the 20-day moving average). Plan your exit at $22.50–$23.00, as the stock faces strong resistance near its 52-week high of $22.80.

But here’s the key question: Are you ready for the risk? If the price drops below $20.50, it’s time to cut losses. This isn’t the kind of trade where you hold onto a losing position, hoping for a miracle.

Long-Term Perspective: Mirage or Real Opportunity?

Let’s be honest: Teva has potential. It remains a leader in the generics market, and its partnership with Alvotech in biosimilars promises interesting prospects. But how can we ignore its massive debt? And the opioid lawsuits? All of this hangs over the company like a millstone around its neck.

A forward PEG ratio of 0.06 is essentially a signal of undervaluation. But that only holds if the company can climb out of its debt hole and stabilize its profits. If you’re considering buying the stock as a long-term investment, it’s wise to wait for a price below $20 to maintain a margin of safety. And yes, this path is for the patient.

Risks You Can’t Ignore

Insiders have a negative outlook, selling more shares than they are buying in Teva Pharmaceutical Industries Limited.

Over the last 100 transactions, 1.64 million shares were purchased, while 2.17 million shares were sold. The most recent transaction occurred 40 days ago, when Roberto Mignone sold 286,000 shares. Overall, insiders are selling more than they are buying. There could be many reasons for this, but in general, it can be considered a negative signal.

The company’s debt burden of nearly $19 billion hangs like a stone around its neck. Legal expenses and regulatory risks, including opioid-related lawsuits, add further concerns. Geopolitical instability, particularly in Israel—where the company operates—intensifies the pressure. And let’s not forget competition: generic drugs are under constant pricing pressure, forcing the company to find ways to stay afloat.

Final Thoughts

Revenue growth is a good sign, but the losses and debt burden are concerning.

If you're willing to take the risk and view this as a long-term investment, the current price might be appealing. However, I’d recommend closely monitoring the company’s efforts to reduce debt and improve profitability.

And here’s the real question: are you ready to wait for this balloon to inflate again?