Udemy: Courses, AI, and Buybacks – Where’s the Money?

The company is betting on B2B: the corporate segment is growing, while regular users are declining.

Udemy (Ticker: UDMY) is one of the largest platforms offering courses for every taste.

Some people learn programming, others try to master the art of negotiation, and corporate clients like large banks and IT companies use Udemy Business for employee training. The key focus is on the business segment and the implementation of AI, which helps personalize the learning process.

Read this first:

Financial report Udemy.

The company has two key business models:

Courses for regular users – anyone can purchase lessons and learn at their own pace.

Udemy Business – corporate training, where large companies educate employees on the latest skills.

Revenue

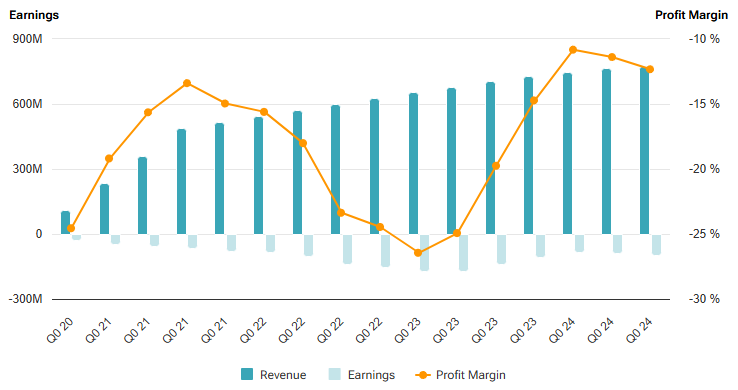

In 2024, Udemy earned $786.6 million (+8% year-over-year). It’s growth, but not impressive. In the fourth quarter, revenue was $199.9 million (+5%), meaning the growth rate is slowing down.

The main growth driver is the corporate segment ($494.5 million, +18%), while regular users seem to be getting tired of online courses: revenue from them declined by 5% ($292.1 million). Could the market be saturated?

It turns out that Udemy is no longer the platform where every knowledge seeker spontaneously buys a course. Now, it’s more of a tool for companies. Is that a good thing? The question remains open.

Profitability

Well, what can we say? Udemy still cannot boast a net profit, but the trend is encouraging. A net loss of $85.3 million in 2024 is, of course, not great, but still better than $107.3 million in 2023. There's an improvement.

Gross profit: $491.9 million (63% margin)

Adjusted EBITDA: $43.0 million (+451% YoY)

EBITDA margin: 5% (vs. 1% in 2023)

EBITDA jumped 4.5 times, but the margin is still small. Maybe the company has finally found a path to efficiency? Or is this a temporary effect, and real profitability is still somewhere on the horizon?

Cash Flows

This part is a bit more complicated. The company improved operating cash flow ($53 million, compared to negative in 2023), but it still spends more than it earns. Net cash outflow – $117.7 million.

Why? It’s simple: $150 million went to buybacks. This means the company itself believes in its stock, but should investors? That’s a different question. So far, Udemy does not generate sustainable free cash flow, meaning it relies on external financing.

Balance Sheet

✔ Cash & equivalents: $355.7 million – a plus.

✖ Capital reduction: $197.4 million (vs. $356.9 million a year earlier) – a minus.

✔ No debt obligations – a big plus.

There is a financial cushion, but the question is: if losses continue, will this cash be enough to reach stable profitability? Or will they need to raise additional funds in a year or two?

Growth Areas

Udemy Business: Growing 18% per year – the company is betting on B2B.

AI tools: Already 1,800+ clients use AI-powered Skills Mapping.

Global expansion: Opened an office in Mexico, entered India through a partnership with Ingram Micro.

Online education market: Demand for learning remains high.

The corporate segment is particularly interesting. Imagine a large bank suddenly deciding that its employees need to improve their soft skills or learn Python. Udemy offers a ready-made solution. The only question is: how long will companies continue paying for subscriptions?

Risks and Challenges

Declining consumer segment: Revenue from individuals down 5%. Could the market be oversaturated?

Competition: Coursera, LinkedIn Learning, Skillshare – competitors are everywhere.

Ongoing unprofitability: No profit yet, and the market doesn’t like long waits.

A little technical analysis. Everyone loves technical analysis:

• RSI: 82.13 (the market considers the stock overbought, a pullback is possible).

• Support: $7.21 (if the price drops there, it could be a good entry point).

• Resistance: $10.61 (if it breaks through, an upward move is possible, but cautiously).

Udemy is playing the long game, betting on business subscriptions and AI. But what if Coursera or LinkedIn Learning find a way to offer something better and cheaper? Then what?

Conclusion

The online education market is growing at a rapid pace. Udemy is well-known and should benefit. The catch is that the company still lacks stable profitability. The platform is popular, courses are selling, but the business model has yet to prove that it can generate sustainable income.

Take Coursera. They have a similar model, but they are already finding paths to profitability. Now look at Udemy: they have been growing for years, but profitability is still out of reach.

And then there’s fierce competition. What’s stopping big tech giants like Google or Microsoft from launching their own courses and taking a chunk of the audience?

For long-term investors, there is potential:

If corporate subscriptions continue to grow,

If AI truly becomes a key monetization factor,

If expenses are kept under control.

Then yes, there is upside. But in the short term, the risk remains high.

Decision? Keep it under observation. A better entry point might come later, when the company proves it can generate consistent profits. For now, just watch.